$9 Bread: The Inflation Debate

A simple view on the gives and takes

I went to the store yesterday to buy bread. A loaf cost $9! I don’t buy bread very often, so maybe that’s not as crazy as it seemed to me at the time, but I couldn’t help thinking about the economy’s hottest topic: inflation.

Everyone is talking about the cost of living as the CPI rose more than 6% y/y in October, the highest rate in 30 years. What makes the inflation debate so fun is that there are smart people on different sides of the argument. Jack Dorsey thinks we’re about to enter a period of hyperinflation, as do many in the crypto community. Cathie Wood thinks we’re going to see deflation driven by technology. Federal Reserve Chairman Powell and Treasury Secretary Yellen had been saying the current spike in prices is transitory, although their tone seems to be changing. Now the party line is that inflation will fade in mid 2022. Legendary investors like Paul Tudor Jones and Jeff Gundlach are arguing inflation might be more persistent, although not hyper.

Howard Marks says the answer about what inflation will do is important, but not knowable. He’s right. The answer isn’t knowable, but we’re all making bets through our investments about what will happen. Bitcoin, in particular, has benefitted from inflation fears. Or at least from people talking about Bitcoin being a good hedge against inflation.

Who’s right, and what should we do about the inflation question?

The Most Important Things

Continuing Marks, not only is inflation not knowable, we also don’t know much about its causes and cures. However, it seems our current inflationary environment is driven in large part by two core factors. Supply chain issues and government policy. If the supply of semiconductors, fuel, and even labor were higher, it stands to reason that prices for many things factored into CPI would be lower. On the government side, accommodative Fed policy continues to encourage demand rather than try to slow it, even as fiscal stimulus has subsided.

Boiling inflation down to supply chain and the Fed may be overly simplistic, but they’re the things most likely to affect inflation for the next year plus given what we know today. Either the supply chain issues will get better, or they won’t. Either the Fed will pursue “good” policy to counteract inflation, or it won’t. Good, in this context means sound policy in the context of macroeconomic theory and perhaps a bit retrospective. We won’t know if policy is good until after the fact.

At this point, good policy almost certainly means raising interest rates sooner, and maybe even faster than expected. As of the Fed’s September projections, members expect the Fed Funds rate to be 0.3% in 2022, up from a 0.1% expectation in the June report. Fed members expect the rate to be 1% in 2023, which is an upward adjustment from a 0.6% expectation in June.

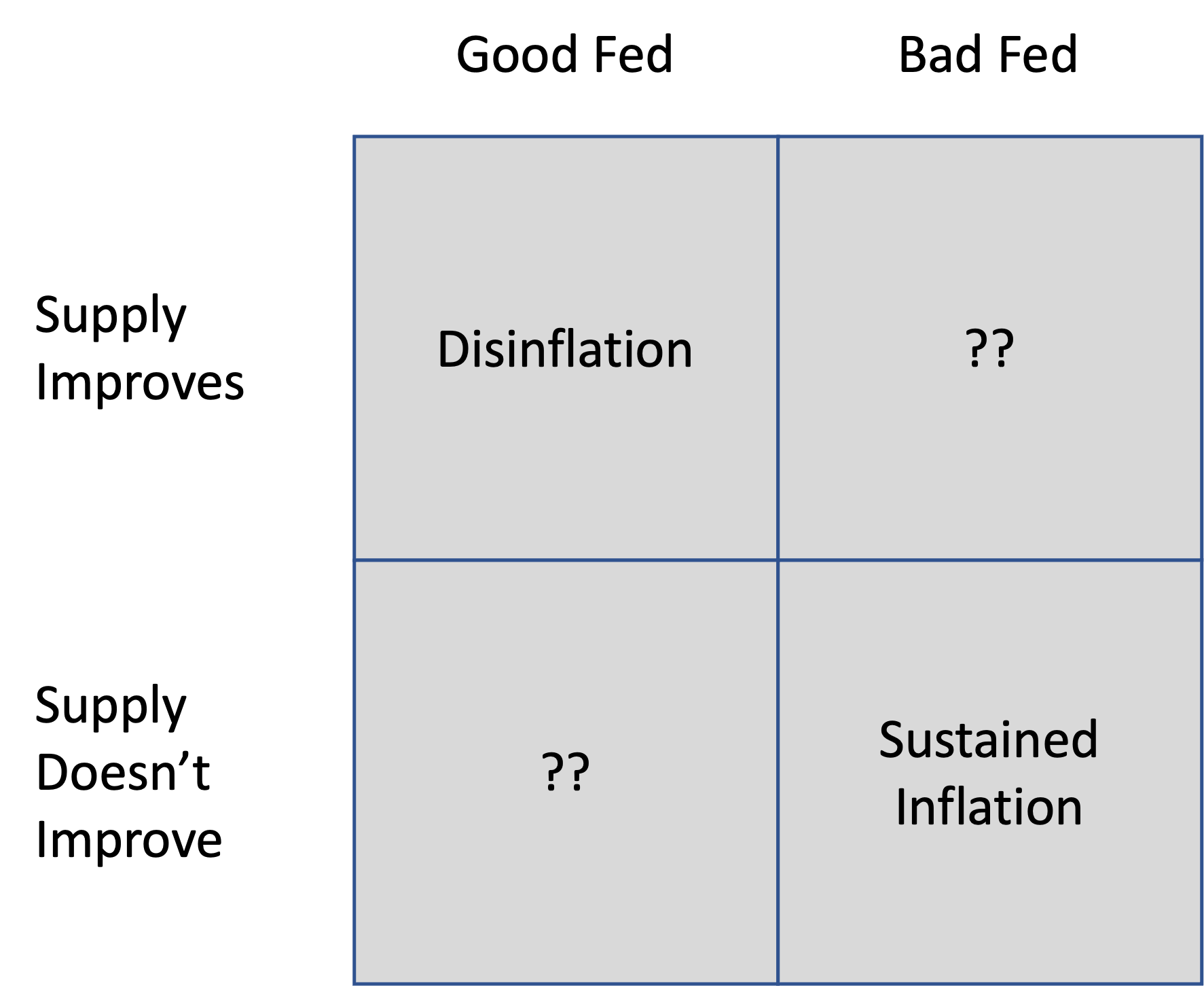

Depending on the supply chain and the Fed, inflation could take a few directions in the foreseeable future:

The outcomes of two scenarios seem obvious.

If the Fed pursues good policy and supply chain issues resolve, we should get disinflation back toward the Fed’s 2% long-term target. I doubt we’d see deflation in this scenario. Wages have been rising, and it’s near impossible to pull wages back. As long as wages remain stable, prices should follow post supply chain issues, at least in the short term. Long term, tech may very well continue to reduce the costs of consumption.

The other seemingly obvious scenario is that if supply doesn’t improve, and we get bad Fed policy, inflation should sustain at a high rate. This would create an even bigger problem to solve down the road.

The other two scenarios have less certain outcomes.

If supply doesn’t improve, but we get good Fed policy, inflation probably doesn’t get worse, but it may not get better. At least right away. Even if supply issues persisted, which would be hard to believe in the long term, interest rate increases would eventually stem demand, although potentially lead to recession.

The last scenario seems most likely to me — supply improves, and the Fed sustains bad policy. At a minimum, supply chain issues probably won’t get worse from here. From an inflation standpoint, that means we should get easy comps at a minimum after a year. More likely, the supply chain improves as there is economic incentive for suppliers to deliver on demand at higher prices.

The reason I’m concerned that the Fed will employ “bad” policy is incentives that have persisted throughout the history of centralized monetary authorities: No policymaker wants to cause a recession during a period of economic growth. Even more so, no policymaker wants to lead us to recession so soon after a global pandemic that wreaked havoc on our economy. On top of the recession issues, the Fed has adopted a mindset of taking more responsibility for social outcomes, which may further delay action relative to considering pure market outcomes.

From this standpoint, it’s more likely that the Fed acts too late and without sufficient aggression in raising rates than the opposite.

But the better supply, bad Fed box is still a question mark as it relates to inflation. Even with inadequate monetary policy, an improving supply chain could result in inflation retreating to prior levels that coincided with loose monetary policy. In this scenario, it probably makes most sense to look for the catalyst for economic calamity elsewhere from inflation, and even then, there may not be a catalyst present.

Uncomfortable Profit

As Marks said, what’s going to happen with inflation is unknowable. There are strong voices that would have you believe this bout of inflation will pass without issue, while other voices would have you believe we’re on a hopeless path to hyperinflation.

When considering the factors influencing inflation, I’m not sure either view is likely. Something in the middle, which is often the case when comparing relative extremes, may be the scenario to embrace. Maybe we have some persistently elevated inflation relative to the Fed’s 2% target similar to what we saw through the mid-2000s. Of course, to the point of looking for economic calamity elsewhere, that era ended in the Great Recession and the bursting of the housing bubble.

The point of this piece isn’t to be alarmist. It’s to be rational. Inflation can be dangerous, and it’s high right now. Those are facts. How it resolves is anyone’s guess but make it a guess based on reason rather than ideology that invites wishful thinking.

I believe inflation is transitory and caused by the Covid Pandemic and its shock to the global Supply Chain and governments' responses. The Supply Chain issue has exposed the California ports and their restrictive trade practices that have caused the bottlenecks. Also, wages needed to rise to help offset the wealth gap. This will be very beneficial. The fact is there is still to much supply in the world and not enough demand, hence low inflation to deflation. And technology has been a deflationary force because of its productivity characteristics.

Excellent! I lived through the 70's and watched my mom and dad go broke on a farm. In 1973, everything looked great, in 1983, everything was 4 times higher, but our goods and services fell behind the devaluation of the dollar. Service on interest killed anyone trying to finance their business, for us buy cattle, etc. However, many did well if they could get govt contracts to build, etc. Consumer goods like cars became crappy reflecting the nations mood. People lost interest in the "quality" of their work, I truly think it began the wealth disparity we see today. I think inflation is 100% govt policy mistakes. My view is that inflation will accelerate until it becomes a 1981 crisis again, because our leaders are so gutless, so pandering to ideology, that we will be forced to repeat history.