What Happens When Consensus Expects a Bad Thing?

How to be contrarian when the market expects the worst

Consensus expectation should yield preparedness. If consensus believes something bad is going to happen, the group will act accordingly. Provided that action has some effect on the outcome, the outcome should be less bad relative to taking no action to stem it. So, from a purely logical perspective, when consensus expects a bad thing, the thing should end up being less bad. The same could be said for the expectation of a good thing. When a good thing is anticipated, the benefits of the good thing are pulled forward. Preparation reduces the bad, hope reduces the good, even if it’s all psychological.

As always, this idea has implications for the broader world, but we’ll view it through the lens of the financial markets.

When Markets Expect a Bad Thing

Why do we care more about what happens when consensus expects a bad thing than a good thing? Because investors become icons when they predict and profit from market collapses. Investing legends are rarely made by riding bull markets. Most investors who do the latter last for one cycle where their strategy fits the current state of the world and psychology of the market, but as those investors fail to adapt to changing markets, they fade to obscurity. The contrarian who plays chess instead of checkers anticipates market collapses and adjusts to the resulting changes in market psychology.

Investors can prepare for a bad thing by purchasing certain assets, divesting others, and hedging. It’s important to understand that consensus is about action, not belief or outcome. If a group all claims to believe something but not act on it, they don’t really believe it. And even with action, the group isn’t always in control of the outcome. Outcomes must be expected for the group to take some action, but that doesn’t mean things will happen as anticipated.

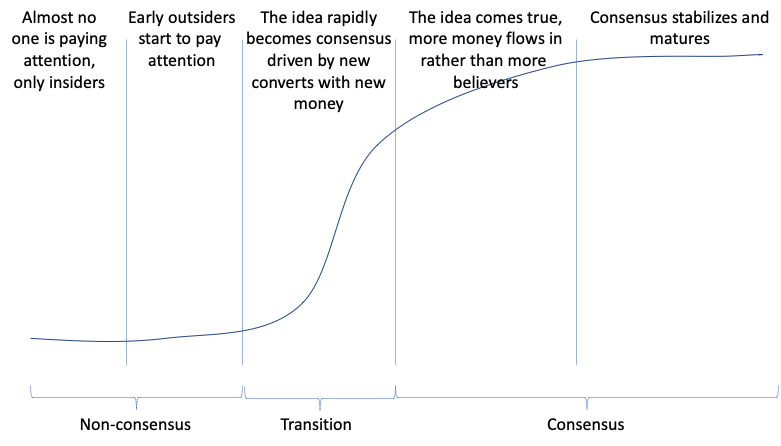

As market participants prepare for a bad thing, prices of the affected assets change. To visualize this, we can return to our progression of consensus graph:

Prices move in the near term as an idea becomes consensus. When prices reflect the expectation of a bad thing, the upside in betting on that bad thing is reduced. The bad thing may still happen, and the bet may still be the right bet, but extraordinary returns don’t come from following consensus.

The contrarian always wants to be different and right, not just different. If the contrarian thinks consensus is incorrectly assuming a bad thing, he can bet against the bad thing happening. It’s particularly contrarian to expect a good thing when the market expects a bad thing. Given the tendency toward human optimism, markets more often expect good things than bad things, so the contrarian more often finds non-consensus ideas in expecting the bad.

If the contrarian agrees with the consensus view of the bad thing, he can explore three alternatives in an attempt to be different:

1. Look for another contrarian idea.

2. Look for alternatives to obvious trades that don’t yet reflect the bad thing in prices.

3. Go further into the trade. In other words, bet on an even worse thing to happen than consensus realizes.

Looking for new contrarian ideas is always the easiest strategy when an investment or trade idea becomes consensus. Refer to the strategies explained in the very first post on tactics for generating new non-consensus ideas. There’s always some good non-consensus idea waiting to be discovered.

It’s the latter two options that are worth deeper exploration. The economy is a complex adaptive system, of which the financial markets are both a component and reflection. Any expected negative economic outcome should have some relatively obvious effects as well as some effects that trickle down to other parts in less obvious ways. Understanding the interconnected bramble bush of downstream effects can offer alternative trade ideas.

Prices reflect consensus, but the less obvious alternative trades may see prices adjust more slowly than the obvious trade. We’ve talked some about the inflation trade here before. Bonds and credit derivatives seem to demonstrate consensus expecting higher future interest rates forced by rising inflation. The upside in that trade is more limited now than it was a month ago, so the contrarian can explore other alternatives with more muted price action to play the inflation trade. Maybe options contracts on gold are underpricing potential volatility. Maybe its currency swaps that provide attractive prices. Maybe there’s something in the art market. In any case, finding these mispriced alternatives to the popular trade can offer extraordinary returns when either consensus gravitates to the asset in question with or without the bad thing actually happening.

The third option is to go deeper into the consensus trade. Maybe the contrarian thinks the bad thing is going to be much worse than consensus expects. In that case, engaging in the obvious trade can still yield extraordinary returns because far more money needs to flow into that idea given the magnitude of the bad thing. While this strategy can work, it really only works for the biggest of negative events, often described later with words like crisis, mania, or crash. The Global Financial Crisis, Savings and Loan Crisis, and Tulip Mania are examples. These events are less rare than a normal distribution might tell us, but still don’t happen very frequently. Normally, the odds of consensus expecting a bad thing and it being worse than expected will be quite low, but that’s what makes going deeper into the trade a contrarian bet.