Volatility and the Contrarian

Charging ahead when others are fearful

Volatility indicates fear, and fear creates an opportunity for the contrarian to do the thing making everyone afraid.

Over the past two weeks plus, almost all the highest-flying names in tech have sold off significantly, especially recent IPOs and SPACs that were speculative favorites. Many are wondering if it’s time to start buying. The answer for a true long-term investor is always that it depends on what you expect regarding the future cash flows for any given company. On that basis, a few of the names may be approaching attractive territory, but that doesn’t mean they can’t trade well below intrinsic value in the meantime.

I believe we’re approaching a generational buying opportunity for some future tech stalwarts, but I’m not sure if we’re there yet. When catching a falling knife, you should always expect to get cut a little bit. You just don’t want to cut an artery.

My excitement for the correction in high-growth tech is balanced with this reality: While the most richly valued names have pulled back, we haven’t seen the kind of clustered volatility indicative of a broad market repricing due to some new fear.

Volatility Clusters

During COVID last year, I studied daily historical S&P 500 returns over long periods. The lesson that volatility clusters ingrained in my mind from that study. It’s one of those things that every investor knows from reading it in a book, but it becomes unforgettable when you spend time living in the raw data that makes it clear how two and three standard deviation daily changes are almost always tightly grouped together. This makes logical sense. When the market is fearful, it should act erratically, searching for some new equilibrium that factors in the genesis of the fear. When the market sees nothing meaningful to fear, it shouldn’t be far off from equilibrium.

By the way, the clustering of volatility applies to life, too. I can attest as my family and I recently left the northeast to move to Florida. The days have been erratic just as they are when you have a kid or start a company or take on a new job. You could argue that successful management of volatility is the basis of contrarianism that leads to extraordinary returns in all things.

Back to investing. When thinking about how volatility clusters in markets, I like to consider the number of two standard deviation daily moves up or down over a 10-day trailing period. When we get to four and five days out of ten, typically we are experiencing some sort of market correction. In the heights of volatility like the COVID period, the 2008 financial crisis, and the Great Depression, we peaked at eight and nine days out of 10 where the market’s daily move was more than two standard deviations from the norm. Consider the Nasdaq since 1986:

In 1987 (Black Monday), 2000 (Dotcom), 2008 (GFC), and 2020 (COVID), we endured clusters of severe volatility that coincided with market corrections. We had similar but smaller blips in 2011 (US credit downgrade) and 2018 (late year sell off).

As of today, only two out of the last 10 days have been two standard deviations from the norm for the Nasdaq. So obviously, we aren’t living in an acute correction, nor have we reached 2011 or 2018 levels of volatility, which peaked at five and four days out of 10 of two standard deviation moves. Even in March of this year we had a 4/10 day period of two standard deviation moves where many of the highest-growth names started their current downward trajectory.

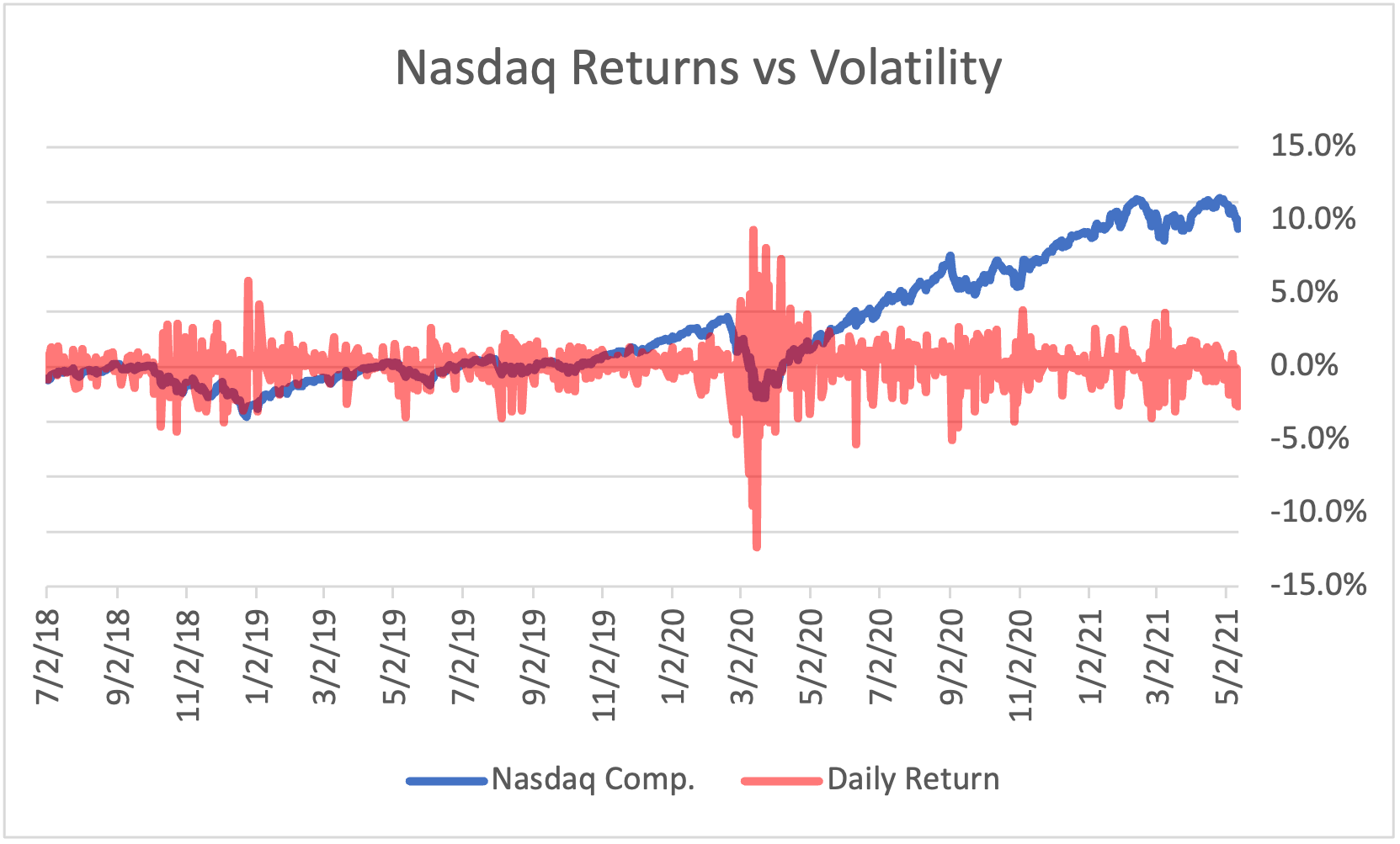

We see this more recently reality if we zoom can zoom into Summer 2018 and forward in the Nasdaq:

Maybe we’re entering a period of broader market volatility off of which we can reset and look to move higher, but the data says we’re not in the middle of it right now despite the pain in high-growth tech.

Putting It Together

It’s possible that investors just started to get some religion around the wild valuations for some of these stocks, and the pain will remain concentrated therein. However, the narrative has been that fear of rising interest rates to stave off inflation triggered the high growth sell off. If true, interest rate fear hasn’t seemed to impact the rest of the market given that we sit near all-time highs with mild historic volatility as described above.

Perhaps the danger is that this volatility is a window into the future. If the broader market did go through a reset to factor in rising rates, the high-growth names wouldn’t be spared from the carnage. They’d probably fall at a faster rate than the rest of the market despite their recent performance. It wouldn’t take another 2000-like correction. A 10% correction in the broader market would probably push many of these names down another 20-50%. That would create the generational buying opportunity I think could happen. The contrarian better be comfortable with volatility to have any chance at being right.

Hi Doug, I really like your thought here! Do you think how likely the S&P500 or market sell off only happen to value stocks excluding hyper growth stock kind of like last year a period of time. I see some of the selling exhaustion from SaaS stocks, they are almost at pre-pandemic levels. Thank you!