Keeping it Real: Loup Edition

Surviving Volatile Markets

Volatile markets test survival, and tech has been the epicenter of volatility this year.

Tech-focused funds have been brutal. Tiger Global’s hedge fund was down 44% YTD in April. Ark’s flagship fund is down 56% YTD. Melvin, not necessarily tech focused, just shut down. Others will probably follow.

Altimeter founder Brad Gerstner found some catharsis sharing that his fund was down more than the market with the hashtag #keepingitreal.

In the spirit of keeping it real: Our tech-and-growth-focused hybrid fund is down mid-teens YTD. The S&P 500 is down 19%. The Nasdaq is down 28%. We haven’t made any new private investments over the past year on valuation concerns. Most of what we hold hasn’t performed well. Entering the year, we held and still hold an uncomfortable amount of cash.

More keeping it real: Being down is always frustrating. I feel frustrated, but given the circumstances, it could be way worse.

Here are three lessons from managing the volatile markets of 2022.

Survival is Underrated

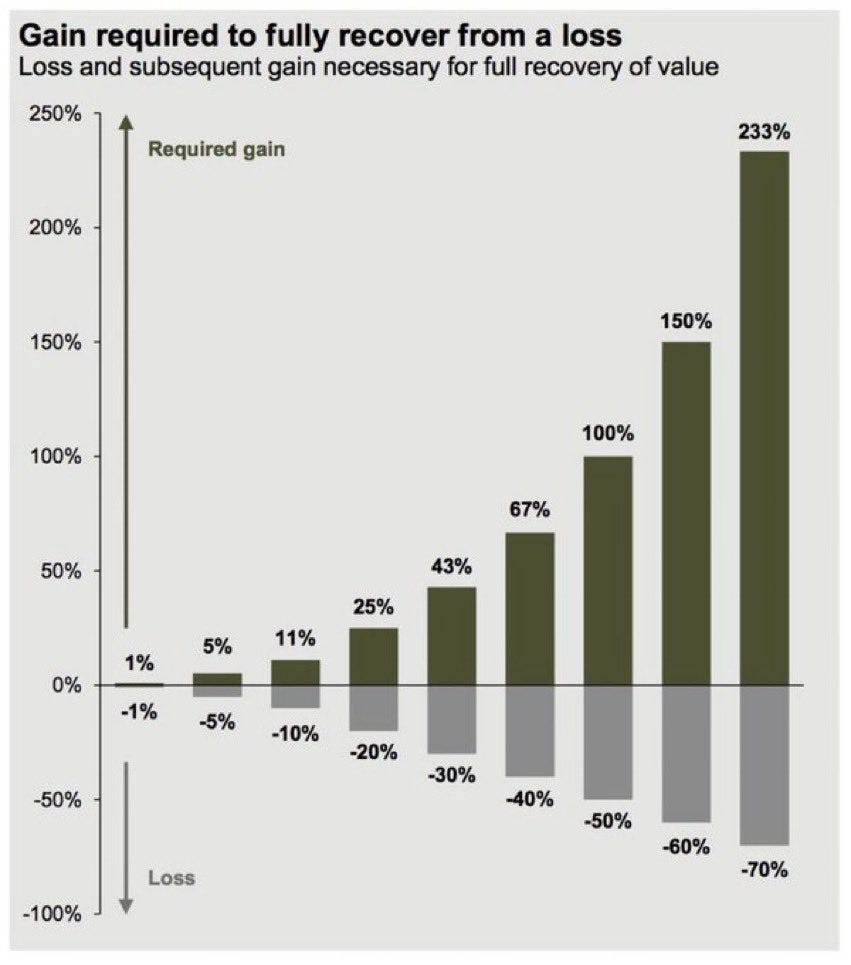

Given the state of tech valuations in 2021, we had one core goal coming into 2022 — survive. Survival demands that you don’t blow up when markets are bad and put yourself in a position where recovery could take years. The bigger the hole you dig, the greater the return you need to get out. In other words, the amount of downside compounds the amount you need to gain on the upside.

Being down 20%, even 30% isn’t too bad. You can recover from that. Being down 50%+ is probably a multi-year battle back to even. Down 70%+…

Everyone wants immediate success and rapid growth, but survival is underrated in all businesses, not just investment management. When others blow up, it creates opportunity for the survivors. If you survive long enough, you maximize your chances for luck to intersect with skill.

Stay Sane

Managing in volatile times is mentally taxing. Even if you get the big picture right, you wish you were more aggressive in your bearishness. If you get the big picture wrong, you wish you didn’t buy the dip for the 10th time.

On top of that, you have bear market rallies, you have names you love and think are objectively cheap that get cut in half, and you have names you love go up 60% in a week before you buy.

You aren’t going to get everything right in volatile periods or any period really. You only drive yourself crazy trying to. There are many things I wish we did differently in 2022, but the big picture is that we’ve survived so far.

Instead of lamenting the little things I wish we did differently, I’m trying to stay focused on the next big thing. What is the next really big thing we need to get right?

This may be taboo for someone being paid to manage money to say, but the less attention you pay to volatile markets, the saner you will feel and the better the decisions you will make. Sanity and mental flexibility are the only ways to capture the big opportunities that volatility ultimately yields after capitulation.

Value and Macro Matter, Duh

The reason we were so cautious toward the end of 2021 and coming into 2022 wasn’t initiated by inflation or the Fed, it was growth valuations. It seemed like every company we looked at was priced like it was going to be the next Google. After about the 100th company we saw with the same mathematical demand of 25%+ growth for a decade, it seemed obvious that things could only end badly. The Fed’s hawkish turn and the battle to stave off inflation was the catalyst for the growth reset. The old advice is worth repeating: Don’t fight the Fed. Especially in a growth bubble.

Valuation work serves better to avoid stupidity than find genius. You’re never going to make a great investment because you built a better DCF than everyone else, but you might avoid making painfully stupid ones.

Never deny the simple fact that prices, and resultant market caps, are a demand on future business performance. A truly great investment will generate far more cash in the future discounted to the present than the current market cap — i.e., it will even greatly outperform your hurdle rate.

Qualitative business factors are what give you the instinct that such business success could happen. Valuation measures only quantify the magnitude of business performance demand.

So, is the volatility done?

I have no idea, and neither does anyone else. Everyone’s bearish. Maybe it’s time to be a contrarian. Or maybe consensus is right.

The best we can do is keep looking at the value offered to us by current asset prices, make some basic assumptions about the macro, and invest when appropriate.

Good luck, stay sane, and do your best to survive.

good read

Yields on 10-yr t-bills just went down. A significant number of investors accept the near certain loss of purchasing power, hoping to buy viable growth stocks at even lower prices sometime in the future.

It may also reflect foreign investors seeking a safe dollar asset vs. their own currency. This makes US growth stocks even more attractive.

And, heck yes, no prediction re timing.