Could a Recession Spark the Real AI Boom?

Investing in AI and with AI is the path through any economic future

The Deload explores my curiosities and experiments across AI, finance, and philosophy. If you haven’t subscribed, join nearly 2,000 readers:

Disclaimer. The Deload is a collection of my personal thoughts and ideas. My views here do not constitute investment advice. Content on the site is for educational purposes. The site does not represent the views of Deepwater Asset Management. I may reference companies in which Deepwater has an investment. See Deepwater’s full disclosures here.

Additionally, any Intelligent Alpha strategies referred to in writings on The Deload represent strategies tracked as indexes or private test portfolios that are not investable in either case. References to these strategies is for educational purposes as I explore how AI acts as an investor.

The Dangers of Consensus

At the beginning of 2023, two-thirds of WEF Chief Economists said a recession was likely in the next 12 months.

We didn’t get a recession in 2023, and the stock market rallied in turn as the assumption of a hard landing turned into hopes of a soft landing. The failure of the recession consensus reminds me of Mark Twain’s timeless advice: “Whenever you find yourself on the side of the majority, it is time to pause and reflect.”

Here we are in 2024. The economy seems strong, inflation seems mostly contained, and we seem to be trending toward a soft landing with some rate relief later this year. At least for now.

Just this past week, job growth reports showed slower than expected hiring while unemployment ticked up to 3.9%, slightly higher than the 3.8% expectation. Could that be a harbinger for the long-delayed recession of 2023?

Maybe, but given the market rally after the weak job numbers, it seems the economic consensus for 2024 remains a soft landing.

Now let’s ask the Mark Twain question we should have asked in 2023. What if the thing that most people expect doesn’t happen? What if we actually get a recession this time?

Surprisingly, it wouldn’t change how I position my portfolio. Here’s why.

AI is Offense and Defense

In mid 2023, when the chances of recession seemed notably higher, I thought the megacap tech stocks were both an offensive and defensive way to stay invested in the market.

If you believed the economy would remain strong, the Mag 6 were positioned to benefit through continued growth in their retail, advertising, and software offerings with optionality from AI adoption. If you believed a recession was coming, the Mag 6 have fortress balance sheets and generate enormous sums of free cash flow each year. In a downturn, the megacap tech companies would be better positioned to weather an economic storm than almost any other company.

The offense and defense narrative still holds for the megacaps, which still aren’t that expensive at a 28.6x forward P/E despite the suggestion of many bears to the otherwise. We’re in a bull market. We’re meant to climb the wall of worry.

But the Mag 6 aren’t the only way to play offense and defense in the current economy. I now believe the offense/defense combination applies to the entire high-quality AI sector that spans both public and private markets.

Reimagine our two economic scenarios, soft landing and recession.

In a soft landing, AI investment continues unabated, and AI is an offensive play that remains on its current trajectory. Hyperscalers will continue aggressive investment in infrastructure. Alphabet, Meta, Microsoft, and Amazon all talked about stepping up CAPEX in recent Q1 earnings reports. Each of the hyperscalers will spend $10’s of billions this year to capture the AI opportunity. Many other Fortune 100 companies will follow somewhat further behind, and a broader set of Fortune 500 companies will grow experiments with AI to improve both productivity/margins and product/revenue. In a couple of years, we’ll start to see the fruits of these efforts pay off for both the providers of AI services and the companies that implement them.

Now let’s imagine we get a recession. Consensus would expect that to slow AI investment, but what if it doesn’t? What if a recession actually accelerates investment into and adoption of AI?

Maybe it’s the contrarian in me, or maybe it’s bias for my belief in AI, but there’s a logical case for why a recession might actually be good for a breakthrough technology that enhances productivity.

The hyperscalers probably invest through whatever economic environment because they have the resources to do so, and we’re in an arms race for the newest technological paradigm shift. It’s incumbent on the incumbents to win, so they must invest now recession or not. AI infrastructure should thus weather any downturn well.

It’s the other companies that might shift behavior in a recession, but I think they might accelerate instead of pullback. Fortune 500 companies largely have resources to invest through a recession too, and it would make sense to increase AI investment to support incremental revenue and productivity as they pare back headcount and other areas as is typical in a recession.

AI investors shouldn’t necessarily root for a recession, but we might not need to fear one either.

Regardless of which economic future we get, I still believe we’re only in inning three or four of the AI boom. Despite the rapid investment in infrastructure to support AI, we haven’t seen AI applications drive meaningful new revenue to most large players, and we probably won’t for the next several quarters.

Whether a stable economy means we stay on the same path or whether economic rockiness fast forwards us an inning, our ultimate destination is an AI bubble. That’s the natural outcome for every game changing technology, and AI will be no different.

Investing With AI in a Recession

While I think investing in AI makes sense whether we get a recession or not, I also believe investing with AI makes sense in the same regard. That brings us to my favorite topic: Intelligent Alpha.

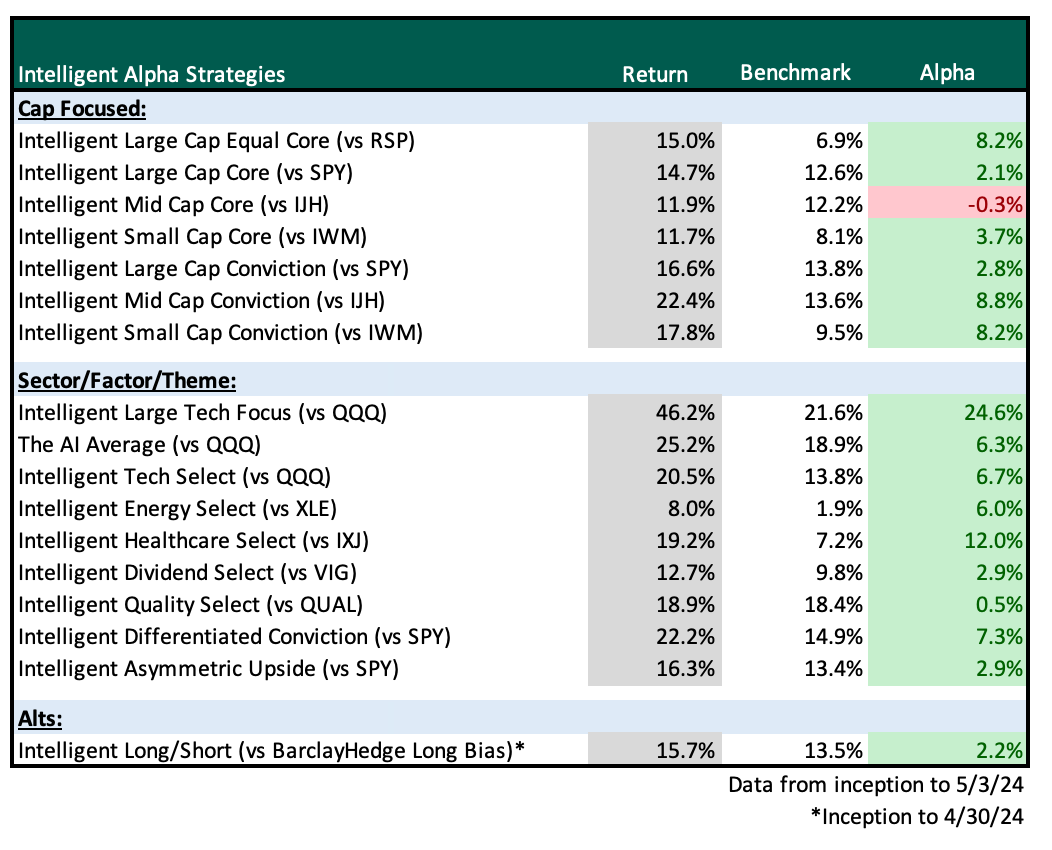

Intelligent Alpha’s mission is to deliver consistently superior investment products powered by AI. To succeed in this mission, Intelligent Alpha’s strategies must beat index benchmarks. Since most human managers fail to beat indexes over the long run, AI wins against humans if they win against the benchmarks.

And Intelligent Alpha (IA) is doing just that.

More than 80% of IA’s 40+ strategies maintain a lead over representative benchmarks with about nine months of testing. The average IA strategy is winning by 370 bps. Amongst the selection of main IA strategies I track, the average win is 640 bps and the median is 620 bps.

The most frequent question I get about IA is some variation of, “Can you explain why AI is winning?”

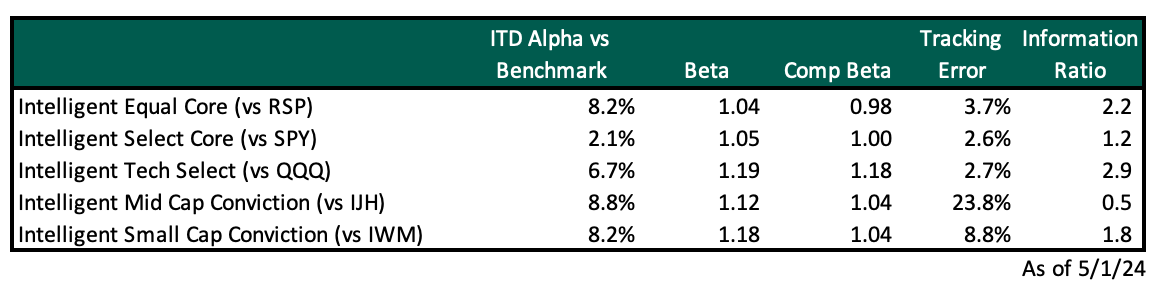

A prospective client asked me this week if I thought beta could also be part of the answer to IA’s performance. I wasn’t sure since I don’t control for beta in building strategies. Instead, I have the AI committee focus on picking what it views as superior stocks. So, I ran the beta to see what the impact might be for a few of the main strategies.

The answer: IA tilts, in many cases slightly, toward a bit more beta than benchmarks, but not aggressively so. Cathie Wood’s flagship ARKK sports a beta of 1.89 vs the QQQ’s 1.18. That’s a heavy beta tilt. By comparison, the 30-stock IA Tech Conviction strategy has a beta of 1.24, nearly the same as the QQQ, and generated +23.7% since mid-September inception to today. Over that time, the QQQ is +15.2% and ARKK is +3.3%.

Like the IA Tech Conviction, many IA strategies have a beta that’s only a few points away from the index. On top of that, the tracking error for many IA strategies is relatively small vs benchmarks, particularly the strategies that are intended to be broader vs more concentrated. I’m particularly proud of the low tracking error those broader strategies show vs benchmarks which results in a strong information ratio given their outperformance.

Sam Altman recently declared that GPT-4 is the “dumbest model” we’ll have to use. Altman also said he didn’t care if he had to burn $50 billion, he’s going to build AGI. Models will only get better from here and quickly.

If Intelligent Alpha can achieve these results with dumb models, what will it do when we have smart ones?

The future of investing is intelligent.

Read more about Intelligent Alpha:

Read one from the archives:

Finding Asymmetries

Every asymmetric opportunity starts with a contrarian idea. If it doesn’t, there’s no asymmetry. The logic is simple: Asymmetric outcomes are a function of supply and demand. If everyone does something, the reward is diluted by broad participation. If no one does something, the reward is concentrated on the few who see opportunity where others don’t. In …