Bull Markets vs Bubbles

And Quant Models vs Generative AI for Investing

The Deload explores my curiosities and experiments across AI, finance, and philosophy. If you haven’t subscribed, join nearly 2,000 readers:

Disclaimer. The Deload is a collection of my personal thoughts and ideas. My views here do not constitute investment advice. Content on the site is for educational purposes. The site does not represent the views of Deepwater Asset Management. I may reference companies in which Deepwater has an investment. See Deepwater’s full disclosures here.

Additionally, any Intelligent Alpha strategies referred to in writings on The Deload represent strategies tracked as indexes or private test portfolios that are not investable in either case. References to these strategies is for educational purposes as I explore how AI acts as an investor.

Bulls and Bubbles

A bull market is a rising tide of investor optimism that encourages gradually increasing stock prices. A bubble is when investors are gripped by mania that results in rapidly rising stock prices that are wildly divergent from fundamental realities.

I still believe we’re in the early part of an AI boom that will culminate in a bubble. Prices aren’t widely divergent from fundamental realities. Yet.

We recently debated whether we’re in an AI bubble at Deepwater. Why isn’t this just an AI bull market? What’s the difference? Why call a bubble a bubble?

As usual, I have many opinions.

1. Evolution

All bubbles start as bull markets. Not all bull markets result in a bubble.

You can’t have a bubble without an initial period of growing investor optimism. You can have a bull market that doesn’t end in a bubble.

Bubbles and technological progress are necessary partners. The Internet, railroads, electricity. Without excessive capital investment, a new technology cannot effectively breakout. Why?

Breakout technology requires two things:

Mass adoption

New products that enable fundamentally new experiences

Excess capital drives down the cost of the new technology to make it widely accessible, ensuring adoption. Excess capital also ensures that every idea is tested, especially the bad ones because they often turn out to be the most profound new experiences.

We’re in an AI bull market, and it might not turn into a bubble; however, if we don’t get an AI bubble, it would only be because we find some flaw in the technology whereby it is not ready to meet its potential.

We should hope for an AI bubble because it would ensure that we get a new technology that improves our lives even beyond the scale of the Internet bubble before it.

2. Psychology

Bull markets are fun (not for bears) and often mistaken for bubbles. Jumpy investors worry about valuation all the way up as assets appear gradually more expensive.

Bubbles are intoxicating and mistaken for new financial paradigms. Investors tell themselves narratives of unrealistic future growth that they discount too far into the future, if they’re even calculating any discount at all. In bubbles, valuations are so silly it’s hard to think about valuation anymore.

The transition between hesitant concern about valuation and ignoring it altogether is the surest sign we’ve moved from bull market to bubble. The market no longer climbs a wall of worry in a bubble. Instead, it scurries up a wall of FOMO.

The optimal investment strategy for a bubble is to invert the mindset of the bull and bubble phases: Act with FOMO when the bull is building and sane investors are worried about valuation, then worry about valuation when the bubble comes and insane investors are gripped with FOMO.

3. Timing

Bull markets can last a long time, many years, even a decade plus. Bubbles, the true peaks, rarely last longer than a couple years.

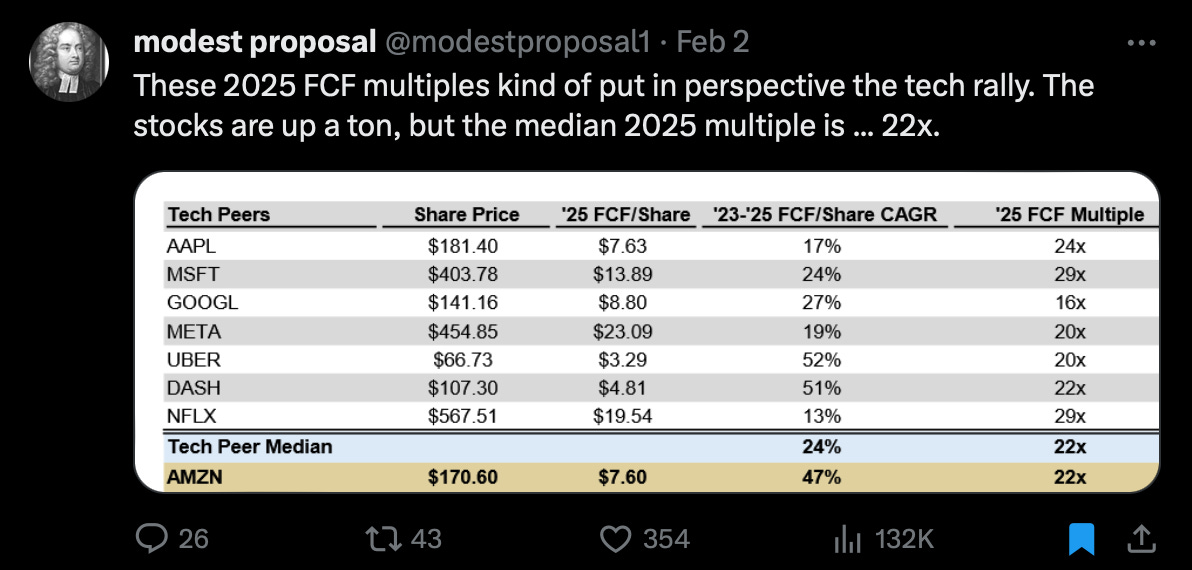

With many big tech stars trading in mid-20x’s 2025 cash flow, i.e. 3-4% yields, it’s hard to say that we’re scurrying up a wall of FOMO despite what stock prices have done. Even NVDA, despite being up 37% YTD already, only trades at 29x FY26 (effectively ‘25) FCF.

The Mag 7 have scurried up a wall of investors catching up to the fundamental realities of the underlying businesses, some of which haven’t even begun to see much impact from AI.

We’re not in an AI bubble yet, and we should be prepared for the many tricks that come along the way. There will be breaks in the bull market; corrections that fool us into believing it’s over prematurely. Counterintuitively, worry that the AI bull market is over is a strong signal it’s not. Conviction that it will never end is when we need to worry we’re deep into the bubble.

For now, BTFD…if we ever get one.

4. The End

Bull markets end in bear markets. Bear markets offer great bargains in a wide range of stocks as the market inevitably turns bullish and starts climbing again.

Bubbles end in crashes. Crashes offer generational bargains for strong companies thrown out with the garbage. Just as you must sell in bubbles when you’ve lost the capacity to worry, you must buy in crashes when markets feel their most awful. We will reach a time in the next several years when we never want to hear the words “AI” again. That’s the time to be greedy.

The funny thing about bubbles is that investor mania is often justified in hindsight. The Internet spawned Amazon, Alphabet, and Meta. It rejuvenated Apple and Microsoft. These are now the biggest companies in the world generating hundreds of billions of dollars a year in cash flow for investors. All the money investors “lost” in the Dotcom bubble has been recouped and more by investors in the giants that benefitted from it.

That doesn’t mean the AI bubble will be different.

We must call a bubble what it is so we don’t lose sight of two things that aren’t mutually exclusive: Euphoria about a new technology can be justified, and investors can pay too much for the fantastic future that will follow.

Disclaimer: My views here do not constitute investment advice. They are for educational purposes only. My firm, Deepwater Asset Management, may hold positions in securities I write about. See our full disclaimer.

Old Quants vs Gen AI Investing

“How is investing with generative AI and GPT different than quant funds?”

I get that question often about Intelligent Alpha.

Answer: Traditional quant approaches and Intelligent Alpha differ in the philosophies dictated by their underlying models.

Quants use machine learning models that feed on massive amounts of data to find trading signals that humans never could. Quant models seek patterns that suggest stock prices can go up, not necessarily why the underlying business should be worth more over time. By nature, quants optimize for trading, whether that be for periods of seconds, days, weeks, or longer.

As Buffett said, the difference between trading and investing is whether you care if markets open tomorrow. If you do, and quants do, then you’re trading. If you don’t because you care about owning the business, then you’re investing.

Intelligent Alpha doesn’t care if markets open tomorrow.

Unlike quant models, foundation models that power GPT and Gemini have a base understanding of the broader world, not the narrow data it’s given. Gen AI’s understanding of the world is not equivalent to a human, but the models are capable of playing the role of thoughtful investor with the right instruction. I teach my AI investment committee a philosophy about investing in high quality companies that should reliably grow earnings over time. It’s focuses on a qualitative, fundamental view of a business first that’s augmented with basic quantitative data.

So far, Intelligent Alpha has proven simple and effective given the results vs benchmarks.

My on-going thesis has been that AI is bound to be a better investor than humans simply because it is not human, specifically that it feels no emotional pull in its decision making. I have a growing belief that most great financial innovations are so great because they eliminate the flaws of human investors more than they find advantages in and of themselves.

Consider indexing and quantitative investing. Both similarly eliminate emotion from the investment process.

Indexes don’t just eliminate emotion, they eliminate all thought beyond the construction of the index. Put in money. Pay low fees. Track the market. Don’t sell. Let the investment grow.

Quant funds also eliminate human emotion by relying on machines to make decisions. Find signal. Trade frequently. Have no memory of whether you’re on a winning or losing streak.

Investing only on index rules or quantitative data loses the element that makes the few great human investors great — an ability to apply qualitative understandings of the world. Buffett isn’t Buffett because he can remember an infinite number of P/E ratios and social sentiment scores. He’s great because he can identify quality businesses across many industries and understand reasonable prices to pay for them. Numbers alone can’t describe the intangible value of the Coke brand or the superiority of an Apple device. Nor can numbers alone convey the duration advantages that come from those qualitative realities.

That’s what makes investing with generative AI different.

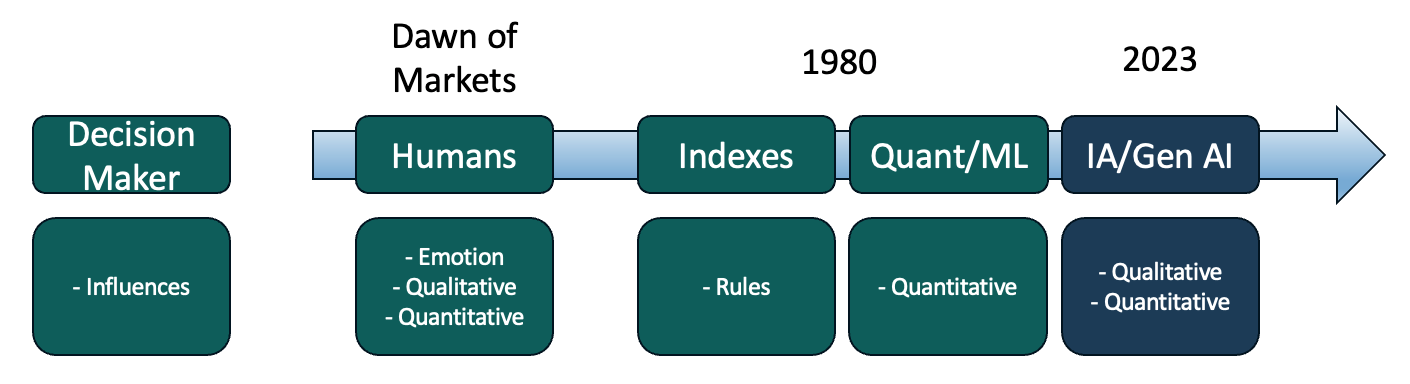

Generative AI removes the emotion that makes for a bad investor, but it keeps the creativity necessary to make unique qualitative assessments of businesses. All of the good without the bad. The evolution from markets driven by humans to markets driven by quants and indexes to ultimately markets driven by general AI is the natural outcome of financial innovation.

Sometimes I get the follow up question, “What if quants adopt LLMs?”

There’s a lot of galaxy brain stuff that happens in quant funds. I’m sure many already experiment with adding LLMs, but I’m also sure there’s a more important question: Do quants want to stop trading and start investing?

My guess is the answer is no. Even if quants did add LLMs to their processes, it’s hard to imagine how they could add meaningful qualitative judgments to trading processes built around quantitative signal. It would require a wholesale change in how they approach investing, and when you try to play a different game, it usually doesn’t end well (see Michael Jordan x baseball).

Sometimes I feel like a peon compared to well resourced quant firms, but I take solace in remembering that the simplest effective approach to any end goal is the optimal approach. Even with my simple fundamental philosophy and my AI investment committee, I’ve seen how AI can outperform markets for more than half a year. Generative AI will only get better from here, and so will Intelligent Alpha.