Benchmarking the Hurdle Rate for AI Optimism

A review of the AI Average Index quarterly rebalance with some bonus AI optimism

Happy 4th of July.

Our AI series continues with a sort of investor’s ode to optimism. We explore the importance of benchmarks in making investments and review the quarterly rebalance of the AI Average Index (AIAI) that I introduced last month. The mission of the AIAI is to establish the preeminent benchmark for measuring financial performance of AI investments. The index is 30 equally weighted stocks with exposure to AI themes in hardware and software, and it’s beating the Nasdaq 100 and S&P 500 handily so far this year.

The Deload explores my curiosities and experiments across AI, finance, and philosophy. If you haven’t subscribed, join nearly 1,500 readers:

Disclaimer. The Deload is a collection of my personal thoughts and ideas. My views here do not constitute investment advice. Content on the site is for educational purposes. The site does not represent the views of Deepwater Asset Management. I may reference companies in which Deepwater has an investment. See Deepwater’s full disclosures here.

The Hurdle Rate for Optimism

Investing is about two O’s: optimism and opportunity cost.

David Senra (Founder’s podcast) has a great quote about optimists vs pessimists:

“Pessimists never make anything. Optimists will have a lot more failures than pessimists but the pessimists just sit on the couch. They never even make it to the line.”

Senra is speaking about company founders who must be optimistic to invest precious time and life to build a company, but the same insight holds for investors allocating precious capital.

Every investment starts with a spark of optimism about some future return. If we’re pessimistic about some opportunity, or maybe even the world, then we shouldn’t invest in anything. Put cash under the mattress, buy some T-bills, and hope the world doesn’t end. Or maybe hope it does.

With optimism in place, we can consider opportunity cost. When we allocate capital to some asset, we don’t allocate that capital to the plethora of other assets available to us. Market benchmarks establish the opportunity cost of making a specific investment rather than buying some basket of exposure.

In a sense, market benchmarks represent the hurdle rate for optimism.

If some investment can’t beat the market rate of return, it’s not worth making. You’re better off channeling your optimism into a general non-specific bet on the benchmark. Owning the benchmark guarantees you don’t lose to the market if you’re not sure you can outperform it.

For a benchmark to be useful, it must be representative of the investment under consideration. It wouldn't make sense to benchmark an investment in AAPL to commercial REITs. Apple is a megacap tech stock with a persistent moat, not a real estate investment. While one might be choosing between AAPL and commercial REITs, a sensible benchmark for AAPL is a basket of the other biggest companies in the world — the S&P 500 for example.

As AI continues to emerge as the defining technological breakthrough of the next decade, it similarly makes little sense to compare an investment in a fast growing AI company to a general set of large cap stocks or even a set of old-line technology stocks. AI investments, whether public or private, should be compared to a benchmark that tracks the value of a basket of AI companies. That’s the true opportunity cost.

That benchmark is the AI Average Index (AIAI) that I introduced last month. The mission of the AIAI is to establish the preeminent benchmark for measuring financial performance of AI investments.

You can track it here.

Why Not Use the Nasdaq 100 to Benchmark AI?

The Nasdaq 100 tracks the 100 largest stocks in the tech-heavy Nasdaq. This includes Pepsi, Costco, T-Mobile, Comcast, and many other non-tech companies. While every company will eventually be an “AI company,” intelligent soda isn’t a good benchmark for the performance AI stocks. I estimate more than 25% of the Nasdaq 100 is weighted to companies with little to no AI exposure.

Further, almost 55% of the Nasdaq 100 is in the Magnificent 7 stocks — AAPL, AMZN, GOOG, META, MSFT, NVDA, TSLA.

While all of those companies have varying degrees of exposure to AI, the weight they comprise in the index makes the Nasdaq 100 more of a tracker of megacap tech than AI. The Nasdaq 100 is not a sufficient benchmark for AI performance because the opportunity set isn’t megacap tech vs an AI investment. It’s publicly traded AI companies vs an AI investment.

The AIAI instead uses an equal weighting across its 30 AI-focused constituents, balancing representation from megacap with with other public companies actively building and marketing AI solutions.

If some idiosyncratic AI investment can’t beat the AIAI, it’s not worth making.

A Review of Q2 AI Stock Performance and Valuation

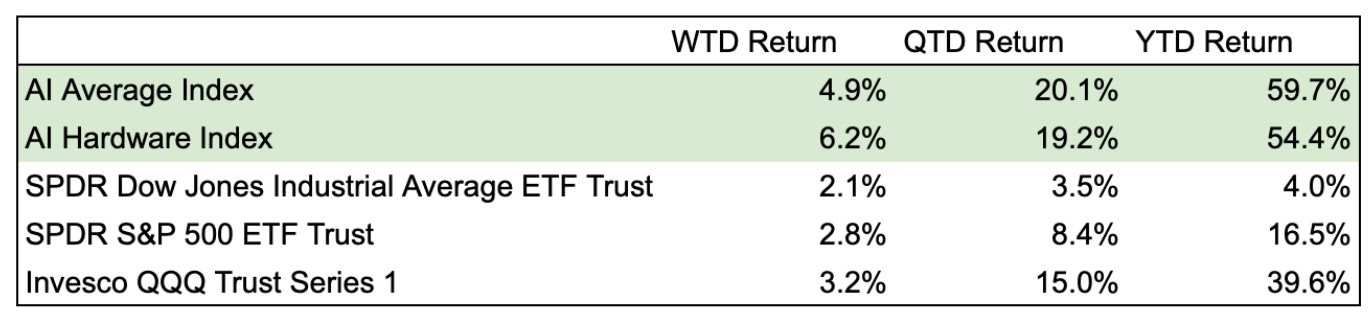

The AI Average Index (AIAI) ended Q223 up 20.1% for the quarter. The AI Hardware Index (AIHI) was up 19.2%. Both indices outpaced the Nasdaq-100 (QQQ) which was up 15% in the quarter and the S&P 500 which was up 8.4%.

As of the start of July, both the AIAI and AIHI have been rebalanced with no change to the constituents of the portfolios. As a 30 stock index, the AIAI goes to a base weighting of 3.33% to start the quarter. The AIHI goes to 4% across 25 stocks.

With the rebalancing in place, the current valuations of the indices appear fair to favorable relative to the S&P 500:

I’m often too conservative in valuing growth stocks even though I’m a “growth” investor. Despite my conservatism, it’s hard to argue that AI valuations feel uncomfortable relative to the S&P, although the S&P’s multiple itself leaves me somewhat uncomfortable. We’re talking in relatives here.

The AIHI feels the most reasonably priced of the three indices at a forward earnings multiple of 26.5x with expected growth of almost 35%. If large tech companies continue to build infrastructure to support large AI initiatives and other large companies outside of tech join them, that growth might prove sticker than expected.

The AIAI trades at a more expected premium to the S&P. It’s hard to argue 55x anything ever feels cheap, but relative to 30%+ EPS growth, it could be worse. At least the AIAI isn’t trading at 20x forward revenue like it’s 2021 again (we’re only 9.4x on that metric).

I’m also a cash flow dinosaur. I like looking at FCF yields to compare owning growth equities to risk-free alternatives. The AIAI currently trades at a 2.2% forward FCF yield, and the AIHI trades at a 3.2% yield. Given a long-term expectation for 3-3.5% 10-year yields, I wish those yields were higher, but in growth we almost always have to buy low yields today fueled by growth that look cheap in hindsight.

What to Expect in 2H23

After a torrid first half for tech in 2023, we’re all curious what markets will bring in the second half. And for AI in particular given its prominent role in the market rally.

I’ll reiterate what I wrote last month about the intense investor interest in AI:

Euphoria, as it always does, convinces believers and skeptics alike that they’re missing out. The result is increasingly less price sensitive marginal buyers who fuel higher prices. But calling a bubble too early only to watch it explode upward can be just as painful as riding one down after it bursts.

Regardless of what happens with AI stocks in the near term, I bet the AIAI outperforms the DJIA over the next decade. AI will provide an investment ground as fertile as the Internet did, perhaps even more so. If you have the aptitude to hold through volatile stock prices, the indices of the future may offer returns better than the indices of the past.

I have no idea what will happen in the second half of 2023, but I am optimistic about AI. With the AIAI, at least I know what the hurdle rate for my optimism is, and if I can’t beat it, then best to just own the index.

Ending on a Note of Optimism

Emad Mostaque is one of the most optimistic voices in AI I’ve listened to. And, to Senra’s point above, founders need to be optimistic, so that’s saying something.

Mostaque is the CEO of Stability.ai which offers the popular Stable Diffusion model. He recently spoke at Peter Diamandis’ Abundance360 conference and offered several optimistic insights about AI:

He believes that there won’t be any programmers in five years. (I think I’d take the over, but eventually he’ll be right).

He expects ChatGPT to run natively on your smartphone within a year meaning it won’t need to connect to the Internet to run.

“Information is valuable in as much as it changes a state. Now we finally have a friend to be with us all the time that can bring us the most valuable information and the most valuable state changes.” He’s referring to AI chat bots.

AI will be able to generate a full movie with our favorite stars in two years.

Google, Microsoft, OpenAI, and Stability will build the base models everyone uses.

Mostaque also said he believes AI is the biggest change in society ever. If done well, that should leave us all with reason for optimism.