3 Takeaways from Instacart's S-1

It's a technology company, and it might be fairly valued

The best way to figure out where the world is going is to experience it.

To that end, I’ve been doing an AI experiment every week to better understand the current major tech paradigm, but this week my experiment was foiled. The idea was to create a dialogue between the recent Instacart S-1 and me using an AI voice clone that I experimented with in my last post. Unfortunately, I ran into some kinks with the voice clone, so I’m sharing the Instacart analysis in classic written form instead.

The Deload explores my curiosities and experiments across AI, finance, and philosophy. If you haven’t subscribed, join over 1,500 readers:

Disclaimer. The Deload is a collection of my personal thoughts and ideas. My views here do not constitute investment advice. Content on the site is for educational purposes. The site does not represent the views of Deepwater Asset Management. I may reference companies in which Deepwater has an investment. See Deepwater’s full disclosures here.

Additionally, any Intelligent Indices strategies referred to in writings on The Deload represent strategies tracked as indexes that are not investable. References to these strategies is for educational purposes as I explore how AI acts as an investor.

Instacart IPO Review

The IPO window is open again. Instacart filed to go public last week, along with ARM and Klaviyo.

I read Instacart’s S-1 over the weekend. Three major takeaways shape how I think about Instacart’s business and the IPO:

Instacart wants you to see it as a tech company, and that defines the core customer and competitive advantage: Create an industry leading omnichannel tech solution for grocery retailers. Investors need to believe in this advantage to get comfortable with the stock.

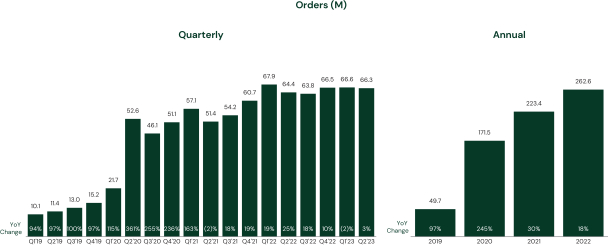

Instacart views order growth as the most important driver of the business, but order growth was flat in the first half of 2023. Investors need to believe order growth will reaccelerate to get comfortable with the stock.

Expect a valuation for CART that would have it trade at multiples similar to UBER and DASH.

Instacart: A Technology Company

When I was a sell-side analyst, we used to joke that every IPO was a tech company because it seemed everyone wanted to tell a story about how they uniquely use technology to command a higher multiple. Look no further than the recent Oddity IPO.

Oddity makes consumer beauty products through a tech-heavy process that leverages data and machine learning to create and market product. The company’s corporate name is Oddity Tech Ltd. In its S1, Oddity states:

We are a technology company seeking to reinvent every aspect of a massive industry. Our tech team is the largest team within our company today and comprises over 40% of our headcount. We invest heavily in data science, machine learning, and computer vision, and we have an evergreen commitment to exploring and investing in emerging technologies. Our technology innovations, when combined with our world-class physical product range and compelling brands built to win online, aim to eliminate significant friction for customers and support a seamless end-to-end user experience.

Consumer-focused companies that push a technology angle always raise alarms for me. Consider the 2021 “tech” IPO of Olaplex, a shampoo company. From their S-1: “OLAPLEX is an innovative, science-enabled, technology-driven beauty company.”

Olaplex’s stock is down 87% from its $21 IPO price.

I don’t know much about Oddity. It may be a great business, but I do know this: Consumers don’t give a shit about technology. Consumers want products that work magically, where technology fades into the background. No amount of technology can save a company with products that don’t inspire consumers and deliver some experience they can’t get anywhere else.

Now Instacart pitches itself as a technology company.

From Instacart’s CEO letter in the S-1 (emphasis hers):

We believe the future of grocery won’t be about choosing between shopping online and in-store. Most of us are going to do both. So we want to create a truly omni-channel experience that brings the best of the online shopping experience to physical stores, and vice versa.

With the business of grocery changing so quickly, many retailers need a trusted partner to help them navigate this digital transformation so that they can drive success both online and in-store and serve their customers better — in all of the ways they choose to shop. It’s especially important because their competitors — from established tech platforms to new startup disruptors — are trying to lure customers away from traditional grocers. If the neighborhood grocer who has been serving their community for decades can’t find an edge, they may not be able to keep up.

That’s where we come in.

Instacart is a grocery technology company.

Should we believe it?

I believe it because Instacart’s primary customer is the grocery retailer, not the end consumer.

Another back on the sell side story: A company IR person once explained to me that the order in which they listed components of the business is how much each component contributed to results. Obvious in hindsight, but it’s a lesson that has stuck with me. The order of things in company reports and filings always tells us something.

Throughout the S1, Instacart lists its constituents in this order:

Retailers — the 1,400 grocers Instacart serves like Aldi, Costco, and Kroger.

Customers — the 7.7 million monthly shoppers who buy on Instacart.

Brands — the 5,500 CPG manufacturers like Campbell’s, Nestle, and Pepsi that advertise on Instacart.

Shoppers — the 600,000 gig economy workers that pick orders at retailers and deliver groceries to customers.

Instacart’s most important constituent is the retailer, and they know it. This may seem a minor point, but it’s important. There are a lot of great companies that deliver groceries. DoorDash, Uber, Walmart, Amazon. DoorDash is gaining share on smaller grocery orders, which makes sense as customers can tack small grocery needs onto other delivery orders with minimal additional cost.

What Instacart’s competitors don’t have is a technology solution built specifically for grocers that creates a deep relationship with those retailers.

The second strength Instacart lists in “Our Strengths” from the S-1:

We are investing more in technology custom-built for online grocery than any single grocer could on their own. Our machine learning algorithms process billions of data points each day to optimize a range of decisions and tasks, including basket building, merchandising, replacements, personalization, ads quality, demand forecasting, order fulfillment, shopper fleet mobilization, dispatching, and routing. Whenever a relevant new technology emerges, we assess how to adapt this technology for the specific needs of the grocery industry and make it available to our retail partners in short order — both online and in-store. We believe this incentivizes grocers to partner with Instacart, as they know that our technology will enable them to transform their businesses and enhance omni-channel customer experiences. Because we do not own inventory, we do not compete with our retail partners. We believe this combination puts us in a unique position to foster greater trust between grocers and Instacart, making us the preferred technology partner.

Technology for grocers is Instacart’s competitive advantage, and it’s particularly appealing to address a customer’s weekly grocery needs. Investors must believe in the value of that competitive advantage to believe in the company and ultimately the stock.

Reaccelerating Order Growth

According to Instacart’s S-1, the total grocery market in the US is $1.1 trillion. Just 12% of grocery buying is done online today up from 3% in 2019 with more growth on the way. From the filing:

Market penetration could double or more, reaching as high as 35% over time. Even then, with at least two-thirds of the grocery market offline, the role of the store will continue to be significant, and it will be critical to serve retailers with technology that enables omni-channel commerce.

Translation: We’re early, and there’s a lot of growth ahead in digital grocery spend just like we’ve seen in e-commerce.

On the theme of listing what’s important, the first thing Instacart lists in its “Key Business and Non-GAAP Metrics” is orders:

We define an order as a completed customer transaction to purchase goods for delivery or pickup from a single retailer on Instacart during the period indicated, including those completed through Instacart Marketplace or retailers’ owned and operated online storefronts that are powered by Instacart Enterprise Platform. We believe that orders are an indicator of the scale and growth of our business as well as the value we bring to our constituents.

Orders makes sense as the most important driver in an early market where consumer activity needs to shift from offline to online, but order growth has flattened for Instacart.

The company explains that beyond some COVID comp issues:

Order volumes have also been, and continue to be, adversely impacted by the effects of macroeconomic conditions, including heightened inflation and rising interest rates, as well as the cessation of government stimulus programs. While we do not expect our pandemic-accelerated order volume growth rate to recur in future periods, we believe we can generate profitable growth in order volume over time.

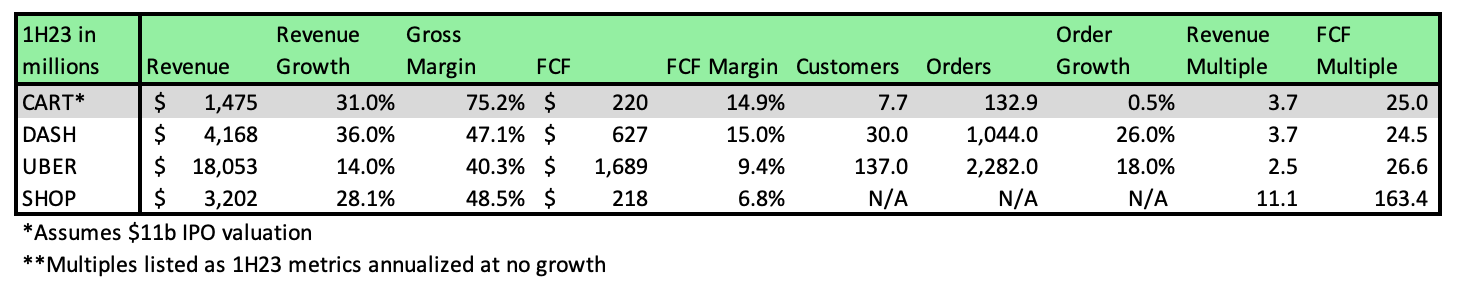

The good news is that despite the flat orders, Instacart grew revenue more than 31% in 1H23 driven by fulfillment efficiencies and advertising:

The increase in transaction revenue during the first six months of 2023, compared to the same period of 2022, was primarily driven by fulfillment efficiencies as we increased our batch rate and reduced shopper incentives that were required during the first six months of 2022 due to the Omicron-driven demand surge, customer fee optimizations, and reduced appeasements and refunds, which also helped transaction revenue increase at a faster rate than GTV.

Although the company cautions that these tailwinds will mitigate:

We expect gross margin expansion to taper in the future as growth in transaction revenue begins to align more closely with growth in GTV.

Despite the same macro and stimulus headwinds, DoorDash grew orders by 26% y/y in 1H23, and Uber grew its equivalent metric by 18%. Perhaps grocery is more sensitive to macro than food delivery or transportation needs, or perhaps we’re reaching a hard part in the adoption curve for online grocery, and incremental customer adoption will be harder to come by.

No matter the case, Instacart has a plan to drive order growth. As always in order of how the company lists its growth strategies:

Attract new customers via incentives and marketing programs.

Expand omnichannel penetration via more in-store technologies like Caper Carts.

Broaden use cases like Instacart Business which helps meet the grocery needs of companies.

Increase access via better affordability and more payment types.

Grow Instacart+ where members spend roughly double non-members.

Acquisitions of emerging grocery technology companies to expand platform capabilities.

Go into categories beyond grocery.

Add international markets.

I think the company nailed the order of growth opportunities from best to worst. A few thoughts:

Every household in the US shops for groceries somehow. With only 7.7 million monthly active shoppers, the most obvious opportunity is to expand the user base. DoorDash has 30 million monthly active users, so the familiarity is there. Investors should expect marketing expenses to elevate to grow orders through more users. Increasing accessibility could also be seen as a marketing cost to the same end.

Instacart+ has 5.1 million members. DashPass has 15+ million members. Uber One has 12+ million members. Amazon Prime has ~150 million. We know that membership creates loyal incremental spend from Prime to DashPass to Uber One. Expect Instacart to get more creative in pushing membership.

Going beyond grocery doesn’t make as much sense when you think about the company’s core competence in grocery and the differing use cases in sporadic buying of things like electronics or sporting goods. DoorDash and Uber, both of whom embrace their role as logistics providers more than Instacart, would seem to have the advantage of being able to deliver non-grocery local purchases at the lowest cost with a similar experience for retailer and customer.

The international opportunity is possible, but major markets are already crowded. Instacart should try, although odds of large success seem limited.

However they do it, investors in CART need to believe that the company will reaccelerate order growth, otherwise the stock is bound to disappoint whatever the IPO price.

A Reasonable Valuation vs Comps

Instacart’s private market valuation reached $39 billion ($125 per share) in craziness of 2021. It’s unlikely the IPO gets anywhere near that valuation.

The company has yet to file a pricing range or the amount of stock it plans to offer, but Instacart states a weighted-average RSU grant value of $35.72 in the S-1. I’ve also heard of secondary transactions for Instacart stock around the $30 range over the past several months.

A $30-35 price for CART would imply something like a $10-12 billion valuation assuming the company raises $500-700 million in the IPO. At that level, Instacart would trade at similar multiples to DASH and UBER.

Looking simply at revenue multiples, one might argue CART at $30-35 appears cheap. Instacart has a higher gross margin than the comp group and is growing as fast or faster, but they also account for revenue differently than DoorDash and Uber. Instacart reports revenue net of the amount it pays to shoppers to pick and deliver groceries. DoorDash and Uber report revenue inclusive of payouts to drivers, so Instacart benefits from

All of this is irrelevant if we just look at free cash flow (FCF), which I always prefer. The further away we get from FCF, the more assumptions multiples must factor in like margins, and the messier they become. A FCF multiple can focus more simply on the growth prospects and duration of the business.

On FCF, the $30-35 range would have CART trade in-line with DASH and UBER, which seems like a fair comparison.

Even though a $30-35 IPO would be nowhere near Instacart’s peak valuation, it would still be a win for the company. Early employees and investors will get liquidity, and Instacart will build on its $1.5 billion war chest of cash to pursue the growth it needs to get back to its peak valuation and beyond.

Disclaimer: My views here do not constitute investment advice. They are for educational purposes only. My firm, Deepwater Asset Management, may hold positions in securities I write about. See our full disclaimer.

Intelligent Indices Update: ChatGPT Still Beating the S&P 500

Back to the idea of playing with new technology being the best way to learn, my favorite AI experiment so far has been creating Intelligent Indices powered by ChatGPT, Bard, and Claude to see if the world’s best AI tools can challenge the market.

Intelligent Indices are performing well vs legacy indices so far.

The flagship Intelligent Select is ahead of the S&P 500 by 10 bps since inception. The Intelligent Tech Select is outperforming the Nasdaq 100 by 100 bps. The Intelligent Select Equal remains ahead of the S&P 500 Equal Weight index (RSP ETF) by 190 bps.

The results show AI is already capable of creating good stock indices with intelligently engineered prompts, and it’s only going to improve over time.

My AI index committee’s big bet vs the legacy indices is going underweight big tech, so the performance is that much more impressive given the strength in tech YTD. If we see any mean reversion in tech vs the rest of the market, the Intelligent Indices are well positioned to benefit.

Instacart isn’t in any of the Intelligent Indices yet. We’ll see whether the AI index committee chooses to add it in the next quarterly reconstitution and rebalance that will happen in September.

The future of indexing is intelligent.

Follow Intelligent Indices on Thematic.